Investment options have often, due to media hype, been restricted to the stock market. The expected answer to any of “Where can invest X amount of money” is, unfortunately, often the stock market or a mutual fund. Apart from the stock market, which appears risky, there are several places where your savings can be invested. Many products are also purchased from a tax saving point of view and that too at the last moment, which often results in wealth erosion. We bring the 5 must-have investments for any professional.

Financial products can be broadly split into two types –equity products that invest in the stock market. This could be direct equity investment or taking the indirect route of mutual funds. Equity returns cannot be guaranteed and if the economy is expected to grow, as in the case of India, then the returns from such products can be very high. Let’s call the investments in stock market as risky investment. The other type is called debt products that invest in lesser violate environment and are often guaranteed by government bonds or well rated corporate bonds. The products here range from Fixed deposit(not exactly debt though), PPF, infrastructure bonds, Government bonds and debt mutual funds. Again, there is no fixed return from debt products, however, the returns are often stable. These can be classified as safer investments.

An investment in any financial product must be a well thought decision. The factors to be considered in an investment must be based on the individual’s financial risk taking capacity and your personal goals. For example, two individuals, Ram and Shyam may work in an IT company and may earn the same salary, but if Ram’s parents are Government employees and Shyam’s are private employees, then the investment options of Ram and Shyam will differ. It would be clear that Ram can take more risks, considering that his parents won’t be as dependent for pension needs as Shyam’s , unless, Shyam’s parents have done proper retirement planning. A working spouse, a dependent sibling, early or late marriage, number of children are other factors to be considered when taking a decision to choose between debt products and equity products. Personal goals ensure that you have a time factor into the investment.

Therefore, amount of money to be invested must be based on an individual’s financial risk taking capability and must have an investment timeframe.

Let’s see the must have investment based on the risk they carry and the investment horizon for the products.

- PPF:

Category: Safe returns, Long term, 15 years investment period.

Who can take: Any age group preferably below 50.

Public Provident Fund has been and will remain to be the favourite wealth creating products when you have to play safe. It comes under the EEE tax regime, which means the contribution, the accumulation and the withdrawal amounts are all exempt from tax. The rate of interest changes every year, but has been hovering around the 8% mark. In a financial year, a minimum deposit of Rs 500 is needed and a maximum of Rs 1.5 lakh can be deposited in PPF. The investment is blocked for 15 years and has partial withdrawal from the seventh year.

Suggested strategy: In your twenties and early thirties, investment as much as possible in PPF to ensure that in your forties you can get a good investment on PPF. If needed, PPF can be renewed for another slab of 5 years to ensure that it becomes a secure source of fund in the beginning of the retirement days.

Common mistakes people do with PPF:

- Invest very little just to cover for tax saving purposes under 80C and not use the Rs 1.5 limit to maximise secure wealth creation.

- Use partial withdrawal from the seventh year. Ideally, PPF should not be touched until it matures.

Tips:

Investment as much as you can in PPF in the month of April to get the maximum interest benefit.

Open a PPF account before moving outside India since NRIs cannot open PPF accounts, but can manage existing ones.

- Equity Mutual funds

Category: Risky returns, medium term, 5 to 10 years investment period.

Who can take: Any age group preferably below 45 and has stable income and less financial burdens.

Equity Mutual funds are the best way for a retail investor (common man) to invest in the stock market. The reasons are simple – mutual funds are managed by professionals and mutual funds invest in multiple stocks usually across industries hence, resulting in what is called as risk diversification. Profits from the sale of equity mutual fund units after a year of holding is free from tax. Since equities are linked to the growth of the economy, it is wise to expect good returns once in every 5 or 10 years. There is no definitive pattern to the ups and downs of an economy, it is usually seen that once a decade there will be at least a boom run, when stock prices soar. When the markets are cruising high, it is best to start selling the fund units to enjoy life.

Suggested strategy: Open an account by visiting the Asset Management Company’s website. If you are not KYC compliant then you need to complete that process which usually takes 2 weeks. If you are already KYC compliant, then you can invest right away from the AMC website. Always select Direct Plans and Growth plans and start an SIP (systematic Investment Plans) in such plans. Based on your risk appetite you can invest as much as 70% of your savings into equity mutual fund schemes.

Split your investment into two categories – one in which you will invest your SIPs for long term (10 years or more) and another you will cash out when the economy is high and the investment period is more than a year. With the tax free profits, you should enjoy the little moments called life!

Common mistakes people do with Mutual Funds:

- Investing in ELSS (Equity Linked Savings Scheme) version of Mutual funds just to save tax and often when the markets are all time high. Ideally, it is best to avoid ELSS for a tax saving purpose. The lock-in period of 3 years can hamper an early exit.

- Investing in lump-sum. It is always wise to buy and sell units of mutual funds over a period of time.

- Checking daily NAV and feeling insecure if the market falls, or dreaming large when the market rises.

- Not buying mutual funds even in the forties, despite a good salary. There is no co-relation between mutual funds and your age – it is all about where the economy is headed. If the economy has dull looks, don’t care about your age, just start the SIPs!

Tips:

Buy only Direct Growth Plans from AMC website. You can save a .75% from the reduced commission of not buying Regular Plans.

Buy Equity diversified, mid-caps and small cap funds as of now. Thematic funds can be avoided.

- Bank Fixed Deposits

Category: Safe returns, 90 days to 2 year time frame.

Who can take: Any age group.

Bank fixed deposits are the best when you have to park money safely for a short period of time. For any time frame of 3 months to 24 months, Bank FD cannot be beaten on the safety factor. So, if you have just returned from onsite with that loads of cash, and unsure what to do, put a bulk of that in an FD for a year and take time to think about it.

Suggested strategy: Invest for not more than 18 months. FD can be a safe source of funds for a short duration while you look around for buying a residential house or other expenses. You can also earn more interest by transferring the money into a senior citizen non-earning parent’s account. But the transfer of money must be for a personal purpose and not merely to save tax!

Common mistakes people do with Bank Deposits:

- Spending too much time on 15G and 15H forms. These forms are to be submitted by those for whom the estimated tax on all income is expected to be nil.

- Putting money in Fixed deposits for more than 2 years. The returns are often comprised due to inflation.

- Checking that auto-renew option. Never do auto renewal. Always assess your financial situation and then take a call on renewal of an FD.

- Trying to invest in parents or spouse’s name without an asset transfer.

Tips

Not more than 18 months should be a thumb rule for getting the best out of FDs

- Real Estate

Category: Slightly risky, 10-15 year timeframe

Who can take: Any age group and has stable income

You maybe surprised, but yes, real estate is still a good means to earn decent returns. But there are conditions – the city or area must be having employment and hence development. Speculative purchases in tier II cities will be only a loss making venture. If you are in a tier I city, with increasing signs of private companies setting up offices, then commercial investment, ie shops, can be a good buy. Rentals are much higher than residential and of course, the cost of acquisition will also be higher. You must have real estate at some point of time in your working career.

Suggested strategy: Try to locate the shops within 2 kms from residential areas or upcoming IT parks. You do get loans for commercial properties but don’t get 80C deductions and the interest rates are also a couple of percentage points higher.

Common mistakes people do with Real Estate

- In case of residential properties, taxation issues can be heavy when a residential property has been purchased on a home loan and sold within 5 years of possession.

- Residential markets in any city are still (as of Jan 2016) way above acceptable valuations.

Tips

Set not more than 40% of your income on real estate investment.

For commercial properties, see if you and a couple of friends or relatives can jointly buy a shop or office floor.

- Debt Mutual Funds.

Category: Relatively safe, 3 to 5 year timeframe

Who can take: Any age group and has stable income

Yes, this is a mutual fund, but instead of equities, ie share of a company, it is on the debt part. Debt mutual funds also have an element of equity in them, but that is usually for dynamic bonds and Income plan funds. Whenever faced with debt mutual funds, you need to choose between long term debt funds and short term debt funds.

Suggested strategy: In a falling interest rate scenario, it may be wise to select a short term debt mutual fund. By holding for more than 3 years, you can also take advantage of indexation of long term capital gains, and significantly reduce the tax. The returns of debt mutual funds will vary, but historically, it has beaten the fixed deposits by a couple of percentage points.

Common mistakes people do with Debt mutual funds

- Assume that it will always give fixed returns.

- Assume that after one year, the returns are tax free just as in equity mutual funds.

Tips

Don’t do SIPs in Debt mutual fund, Invest in a lump sum.

Stay invested for minimum of three years to take advantage of indexation of tax outflow.

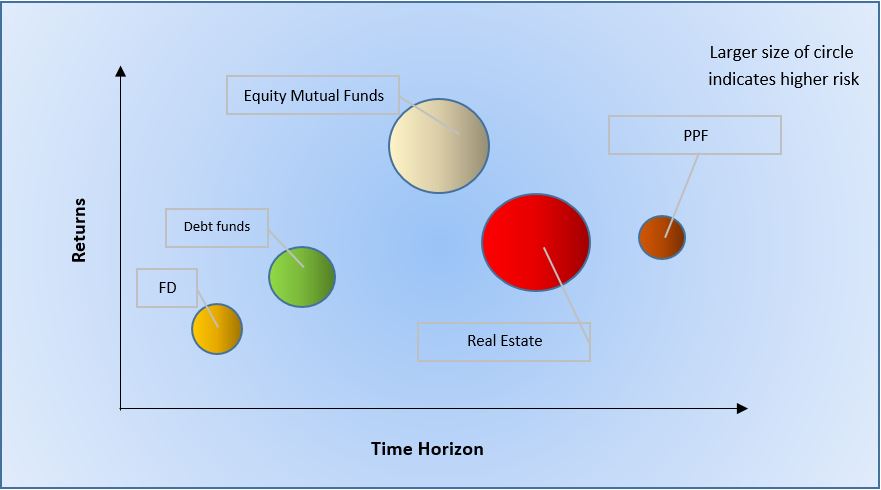

Summary:

You can take a look at the diagram!

[About the Author: Krishna Rath is a SEBI Registered Investment Advisor and the founder of the finvestor.in, a website to help you get the best financial advice. He can be contacted at [email protected] ]